The IIRC’s founder and Chair Emeritus, Professor Judge Mervyn King, recently said that “business is a part of society, not apart from society”. This message has never been more relevant than in 2021.

Business resilience continues to be strongly tested in the wake of the Covid-19 pandemic and, as the World Economic Forum’s 2021 Global Risks Report revealed, rising socio-economic inequality and the challenges of environmental sustainability remain the context for the year ahead. The systemic scale of these risks poses challenges for organisations’ boardrooms. At the heart of decision-making and implementing real change, a board needs to establish in the development of its company’s business model and strategy: what is the company’s purpose? Who does it serve? And how can the company create long-term value for all its stakeholders?

Boards have a crucial role to play in taking action to understand and articulate the context within which the business operates. Purpose-driven companies in 2021 will be far more resilient because they will have a stronger connection to the legitimate needs and expectations of their stakeholders, and understand how their purpose interacts with the world around them, emerging trends and how their relationship with a variety of resources, or capitals, helps to create value over time.

Stakeholders and business resilience

2020 highlighted the importance of recognising the value of employees, clients and customers, suppliers and shareholders, to safeguard a business’s financial stability and sustainability. Due to the Covid-19 pandemic, businesses reprioritised their employees’ safety and wellbeing over short-term profitability, ensuring office-based workers could work productively from home and that extra safety measures were put in place in the workplace for staff and customers.

With the Covid-19 pandemic continuing to disrupt our everyday lives for the foreseeable future, it is vital that companies support their employees and customers in ever more innovative ways. Where many employees are feeling siloed and isolated, many boardrooms are embracing digitalisation to bring people together.

For example, the Dutch multinational bank, ING Group, is forging ahead of the curve. With the help of integrated thinking, the ING Board established a clear whole picture view of their stakeholders in their business model and strategy which, in light of the Covid-19 pandemic, has meant they are well placed to support them all. ING put into place guidance and infrastructure for remote working, offered online activities, social events and wellbeing surveys to see how their employees are coping.

ING is also supporting its customers in offering hybrid model remote advice, including human interaction, video calls with clients, and increasing outreach through podcasts and webinars. Such digital engagement is not only effective at cementing an understanding of organisational purpose and strategy but also in fostering business resilience, by making all stakeholders feel part of a community at a time when they might feel most isolated.

Board diversity brings value

Diversity and inclusion at board level are increasingly becoming financial, as well as moral, obligations. Fair representation at board level is vital in ensuring boardrooms are equipped with the skills needed to adequately understand and meet the needs of their diverse stakeholders.

State Street, one of the world’s top three asset managers, has announced that it will vote against certain board nominees at companies that do not disclose diversity data, with BlackRock also conceding that it may do the same.

With the dawn of the new Biden administration setting a new political contour lines by promising a focus on greater diversity, and the swearing in of Vice President Kamala Harris, the first woman and first person of colour to hold the nation’s second-highest office, visible change is already taking place. Against this backdrop, there has never been a better time for boards to evaluate their own effectiveness and ensure that each member is bringing value to the table.

The risks of climate inaction

In the Reith Lecture 2020 series, Mark Carney delivered a striking comparison in attitudes towards how we value business and the environment. The former chair of the Financial Stability Board, who is leading private sector preparations for COP 26, asked how we can we place more value on the e-commerce giant Amazon, which is now valued at over a trillion dollars, than the rainforest from which it was named, which provides 20% of the world’s oxygen and suffers devastating deforestation on a daily basis.

According to the World Economic Forum’s Risk Report 2021, climate inaction poses the largest risk to the planet, from fire and extreme weather conditions to rising sea levels and more. It is therefore up to every business to address the climate crisis and put in place proactive measures to help combat it.

Integrated thinking is a transformational governance tool that boards are using to connect their organisation’s strategy, performance and culture to the external environment, in order to set achievable goals around sustainable development and responsible capitalism. Initiatives and goals to combat the climate crisis, for example, are born in the boardroom and entrusted to every stakeholder in the organisation to implement and make a reality.

Companies are using the IIRC’s IR Framework to understand the interconnectivity of capitals, with an emphasis on the balanced reporting of outcomes, value preservation and erosion scenarios. In the case of Munich Airport (FMG), for example, the IR Framework has helped identify an overview of all the airport’s inputs, outputs and outcomes, especially towards the environment. The airport’s integrated approach has resulted in greater transparency of reporting and key performance indicators to measure the success of sustainability initiatives, such as achieving the UN’s Sustainable Development Goals, as well as reaching their own goal of being carbon neutral by 2030.

An integrated solution

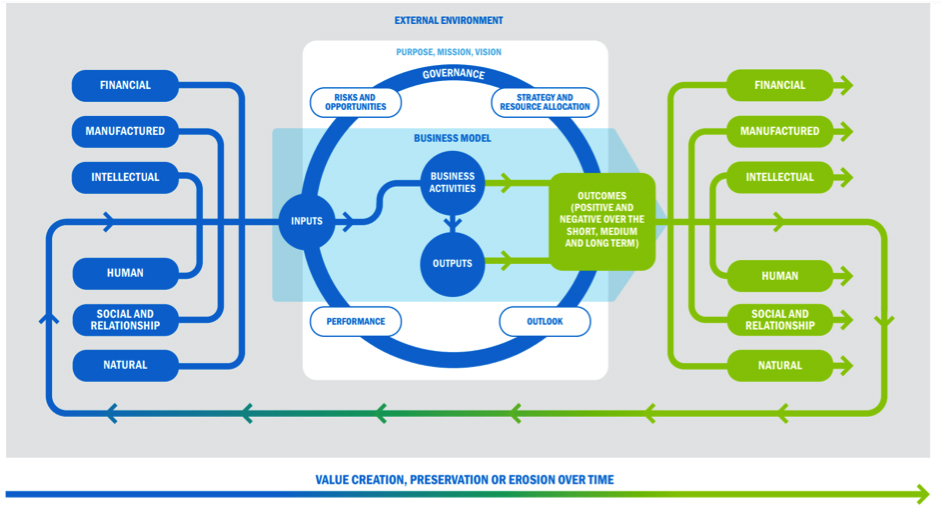

The IR Framework offers a structured approach to integrated reporting, helps organisations through a multi-capital approach to corporate reporting, placing equal weight on financial, manufactured, intellectual, human, social and relationships and natural capitals. By gaining a holistic overview of the business’ inputs, outputs and outcomes, boardrooms can develop an understanding of how their business dynamically interacts with all capitals to create value over time (see graphic below). This, in turn, is connected to long-term investment, which is key to sustainable development and business resilience.

The scale of these challenges, and the growing demands they place on boards to make fundamental changes to their organisations, will not be overcome overnight. However, understanding how these relationships interact to create value enables effective decision-making and allows boards to address the systemic challenges facing the 21st century. This transformation of thinking can have dramatic implications for the success of an enterprise, moving business decision-making from reactive to proactive, replacing short-term thinking with long-term value creation, and enabling companies to create prosperity for themselves, their communities and the world around them.

Integrated reporting has now been adopted by over 2,500 organisations in more than 70 countries, which shows that a multi-capital approach to corporate reporting is here to stay.

Jonathan Labrey is chief strategy officer at the International Integrated Reporting Council.

Related Posts

-

July 14, 2022

Among its complaints, the Business Roundtable argues that no ‘safe harbor’ in the rules will increase the risk of corporate liability.

-

October 27, 2022

Company cashflow reporting; workers on boards; country-by-country tax reporting; FTSE companies and ethics; US corporate crime database.

-

March 11, 2022

The Big Four leave Russia; Apple investors call for "civil rights audit"; UK firms aim for gender parity; and trend grows for four-day weeks.

-

December 10, 2021

Jon Moulton defends UK audit; Colin Mayer on business schools; more women on S&P 500 boards; FRC looks ahead; and how ethical are you?