In 2021 the European Commission will present two intertwined legislative proposals aiming to foster integration of sustainability in corporate strategies. The first one, the reform of the EU Non-Financial Reporting Directive (NFRD), aims to ensure transparency on companies’ sustainability performance to improve corporate accountability and enable sustainable finance (see our previous article). The second one, the sustainable corporate governance initiative, will clarify corporate obligations to identify, prevent and mitigate severe human rights and environmental impacts, and board oversight over sustainability risks, strategy and targets.

Such a combination of transparency and governance incentives, together with the push of responsible investors, will reinforce the market pressure for companies to elevate the consideration of sustainability among managerial and board priorities, while granting companies considerable flexibility in how they do this.

EU Commissioner for Justice Didier Reynders explained the second initiative to be launched this year, during a recent event organised by Frank Bold and CDSB, by stating: “Environmental degradation and climate change are creating risks to businesses and their supply chains. The transition creates big opportunities and companies that are ahead in the game will benefit most. We want to ensure that corporate decision-making changes to a sustainability mindset at all levels. “

Access to the right data is the key for companies and their boards to consider material sustainability risks and opportunities in their strategic decision-making, including those linked to the transformation of the European economy towards a low-carbon model.

Currently, a vast majority of companies do not show signs of considering such data, as evidenced by the state of reporting on sustainability from a strategic business perspective. For instance, the analysis of 1,000 large EU corporations’ non-financial (sustainability) reports by the Alliance for Corporate Transparency revealed that, on average, only 14% of companies provide insights on the integration of sustainability in core business strategy, Board discussions, and performance incentives. A follow-up study on the climate reporting of 300 Southern European and CEE companies from high-risk industries showed an even bigger gap, with results between 7.2% and 10.6%. Forward-looking information on companies’ strategic targets and progress is disclosed by less than 10% of companies for climate transition plans, and less than 4% with respect to human rights risks identified by the company.

In the first part of this article, we explain how the governance of sustainability matters helps companies to identify material sustainability information, and how such data enables companies and their managers to properly consider risks and opportunities and make strategic decisions.

In the second part, we provide an overview of the three areas of information on governance and integration of sustainability that the reform of the EU Non-Financial Directive will seek to clarify (in line with leading existing standards), which are critical for the success of company’s reporting and communication with investors:

1. Company strategy and targets and board oversight over their adoption and implementation

2. Determination of relevant risks and salient issues (double materiality)

3. Organisation and integration of sustainability in governance

Governance in sustainability: the reason behind the EU Commission’s proposals

Directors’ associations, business organisations and investors, increasingly recognise the urgency of the climate crisis and the need to fully integrate sustainability and respect for human rights in companies’ business models and risk management. The sustainability crisis and the challenge of ensuring recovery from the Covid-19 crisis are of an unprecedented scale and urgency, as highlighted by Commissioner Reynders who also stressed that “companies that are ahead in the game will benefit most”.

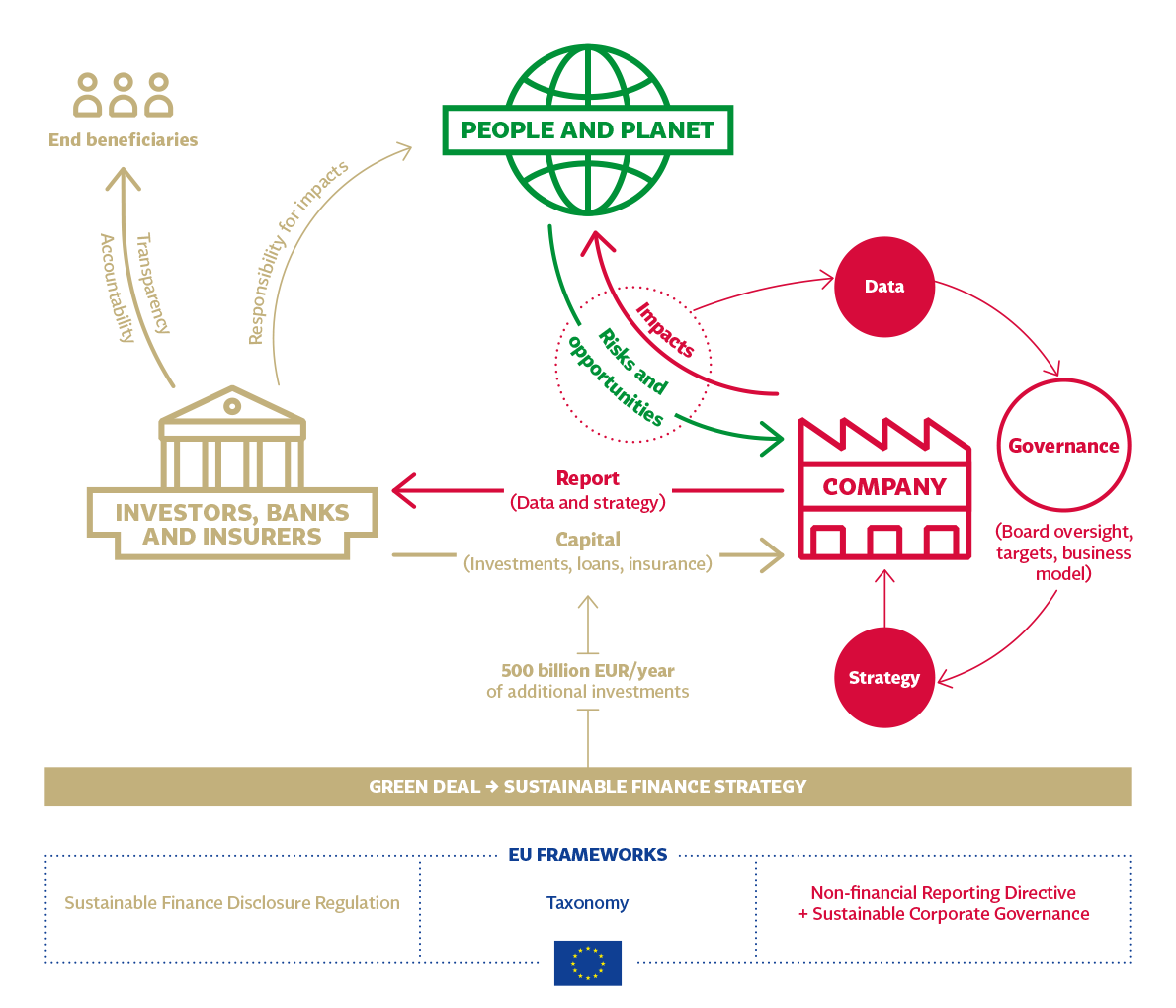

According to an estimate from the European Commission, at least half a trillion euros of additional investments per year will need to be redirected from business-as-usual to sustainable activities. The risks and opportunities linked to the realignment of finance and markets are therefore equally unprecedented.

The need for effective governance and oversight from the company’s most senior governing body and integration of sustainability is proportionate to the challenges facing companies. This is particularly relevant where risks and impacts are connected to the company’s business model, as this will in turn require major changes to the strategy and financial planning.

The International Corporate Governance Network (ICGN) is currently updating its Global Governance Principles, and as George Dallas (its policy director) highlighted at an event this February, there will be a “big emphasis on the themes of boards become developing understanding of not only how ESG factors impact them, but on how their company impacts society in a broader context (…) this, in turn, leads to the need for good information and metrics to guide both executives, board directors, as well as give investors clues in terms of where opportunities and risks might lie.”

As the Alliance for Corporate Transparency research on corporate sustainability reporting shows, the problem is that sustainability information is often invisible to corporate decision-makers, which makes it impossible for companies to make fully strategic decisions. Furthermore, from the point of view of investors and lenders, sustainability information is of little value if it is not clear how it is used by the company and reflected in strategy.

Larry Fink, founder and CEO of BlackRock (the world’s largest asset manager), in his notorious annual letter to CEOs, is directly asking companies in their portfolio to “disclose a plan for how their business model will be compatible with a net zero economy. We are asking you to disclose how this plan is incorporated into your long-term strategy and reviewed by your board of directors”.

Along similar lines, Rients Abma, executive director of Eumedion, an organisation that represents the interests of institutional investors with investments in Dutch listed companies also stresses that: “Sustainability risks and opportunities will impact the company’s ability to create long-term value and to promote the company’s long-term sustainable success. Consequently, proper and knowledgeable board oversight on these subjects and meaningful reporting on the execution of that duty are extremely important for institutional investors”.

Diagram: Reporting, strategy and governance framework for sustainable finance

The need for a strategic approach to climate change and human rights

With respect to climate change risks, it is paramount that energy producers, manufacturers with high greenhouse gas emission intensity, and banks and investors urgently chart their long-term transition plans to survive—and ideally thrive on—the major market changes just beyond the horizon.

A recent study by CDP showed for example that European companies had identified €1.22trn in new low-carbon business opportunities, such as through higher demand for electric vehicles and green infrastructure. The value of these opportunities is more than six times the investment cost of €192bn. Yet, Alliance for Corporate Transparency found out in its 2020 research of 300 European companies that less than 17% explain business opportunities related to sustainability challenges.

A critical step for companies to prevent or mitigate sustainability risks and impacts, is the adoption of targets and proper ways to monitor progress and results.

Alberto Carillo Pineda, co-founder of the Science-based Targets Initiative, confirmed that a growing number of companies are asking their suppliers to set science-based targets and noted how this would be a key component to accelerate their adoption and institutionalise the practice. In addition, he stressed that other actors and initiatives are pushing towards the same goal “All of these are necessary ingredients to really create an enabling environment and to make SBTs and the adoption of sustainability targets and strategies that are in line with planetary boundaries, our goals, a common practice.” The Alliance research positively noted that, in the last two years, there has been a 20% increase in companies reporting science-based targets (improvements are concentrated in Spain with 41% of companies disclosing this type information, reflecting the clarification in the Spanish transposition of the NFR Directive that companies should disclose their climate targets)

A strategic approach to the governance of sustainability is also required where companies are connected to severe human rights and environmental impacts through their value chains. Companies will be increasingly expected by market mechanisms and by the law to assume responsibility in this area. In order to achieve the objectives set in the European Green Deal, severe impact by companies to society and the planet need to be mitigated, rather than perpetuating the current model of externalising and dissolving responsibilities across global supply chains. Such systemic problems include large scale deforestation and land grabbing linked to agricultural commodities such as soy, beef and palm oil; exploitation of workforce in garment and footwear supply chains or abuse of technologies by the clients of ICT companies.

Théo Jaekel, corporate responsibility rxpert at Ericsson, is crystal clear in his support for the EU plans to introduce mandatory due diligence requirements: “We need to go beyond disclosure and move to the management of risks. It is important to see this kind of legislation as an opportunity, and not as a burden because it can clarify how the responsibility of companies looks like in the entire value chain in comparison to current uncertainties around how far-reaching responsibility is, and what can we actually expect from companies. If done correctly, it will alleviate these concerns”.

With regards to board oversight and management of sustainability issues, Jaekel sees this as a crucial part of embedding due diligence requirements, rather than an issue to be solved by changing directors’ duties. “The targets we set at a group level, including environmental and human rights targets, are approved by the management and the board, their results are reported back to the board on a regular basis”.

John Ruggie, author of the United Nations Guiding Principles on Business and Human Rights, has recently explained the connection with human rights due diligence as follows: “By making HRDD mandatory, with penalties for non-compliance as the EC intends, it becomes a legal responsibility not only for management but also for board oversight.” In this context, investors as well as leading reporting frameworks, increasingly expect transparency on board oversight over due diligence and materiality determination processes and how the results of these processes are reflected in the company’s strategy as a whole.

How can companies better report the ‘G’ in ESG?

Reporting on the governance related matters concerning sustainability is addressed by leading reporting standards, including GRI, SASB and CDSB, as well as in the benchmarks developed by the World Benchmarking Alliance. The Recommendations of the Task Force on Climate-Related Financial Disclosures, the standard for climate reporting endorsed by the international investors community as well as by the European Commission, includes board-level governance of an organisation’s climate risks and opportunities as one of the four main areas for disclosure. Similarly, the UN Guiding Principles on Business and Human Rights require the involvement of the most senior level of a company’s governance in discussing its salient human rights challenges, policies and targets, and in tracking progress.

The EU Non-Financial Reporting Directive requires companies to disclose strategic information, but it fails to provide clear guidance on how to determine which information is material and how to select relevant data and metrics from existing sustainability reporting initiatives and standards, which together include over 5000 highly divergent KPIs. This, combined with proprietary questionnaires of rating agencies, investors and buyers in the supply chain, makes it very difficult for companies to approach reporting and sustainability from a strategic perspective.

In reaction to these problems, the reform of the EU Non-Financial Reporting Directive (see our previous article here) will aim to help companies by clarifying which information should be reported on governance and integration of sustainability in corporate strategy. The European Project Task Force on Non-Financial Reporting Standards under the EFRAG has recommended in its final advice to the European Commission that future EU reporting standards should include a standard on “Strategy”, to be structured under three components: a) overall business strategy b) material sustainability risks, threats and opportunities and c) sustainability governance and organisation. This overarching standard should be then supported by topical standards, for example on climate-related information, addressing implementation (policies and actions) and performance measurement (achievements and progress measured by KPIs).

Three essentials for disclosure on governance matters

In the three areas of strategic and governance-related information, there are several categories of information which are critical for the success of a company’s sustainability strategy and reporting, are already expected by leading reporting standards and large investors, and will become increasingly important for companies at the top of value chains:

1. Business strategy and board oversight

The law provides board members with wide discretion to consider sustainability when making decisions on behalf of the company. In this regard, the following information is critical to understand how a company integrates sustainability at strategic level, and for boards to have access to relevant data:

- Board-approved strategy to address salient sustainability issues, including specification of:

- High-level measurable targets relevant for the prevention or mitigation of risks and impacts for each salient issue identified by the company

- Financial resources approved for the implementation of the strategy

- Revisions to the company’s business model, strategy and financial planning

- Progress report about meeting the targets and challenges, signed off by the board

2. Double materiality determination and due diligence

Integration of sustainability in business strategy rests on a good understanding of which sustainability issues are material. The EU NFRD builds on the ‘double materiality’ perspective, which provides directions to companies on how to identify issues which either:

- already have or may lead in the future to financial risks and impacts for the business; or

- represent the areas in which the company is causes, contributes to, or is directly linked by business relationships to severe impacts on people or the environment across its value chain (the determination of such issues is the first step of the process of human rights and environmental due diligence, which is supported by robust guidance and which will be covered in detail in one of our next articles)

In this regard, key information is the following:

- A description of the process and principles applied by the company to determine its material issues, including information on how affected stakeholders were consulted (according to human rights due diligence, companies should engage specifically with people who are at risk of harm due to how a company does business, rather than general categories of stakeholders such as customers, communities, etc. The need for engagement is proportionate to the risk and severity of the harm)

- A description of sustainability issues determined by this process alongside an explanation of why the issues are deemed material from either the financial or impact perspectives

- Details of the company’s exposure to risks or involvement in impacts for these issues.

Currently, a majority of companies report on issues which are not relevant from neither the financial nor the impact perspective, and provide no information on the materiality determination process. Typically, companies fill their reports with information on philanthropy, volunteering, and other CSR activities which are additional, rather than linked to their business. Companies’ reports often suggest that topics covered are selected because the company perceives them as being expected by their stakeholders, but fail to explain whether those topics are in any way material.

3. Sustainability governance and organisation

The extent to which sustainability considerations are integrated across a company’s governance tools underlines its ability to reflect them in business decisions. To ensure and demonstrate to investors that sustainability is integrated, leading international standards such as the TCFD highlight three priorities:

- A description of how the determination of sustainability issues based on a double materiality approach is integrated in the broader enterprise risk management system. Companies need to demonstrate that these systems not only reflect sustainability risks to the company itself, but also risks it poses to affected stakeholders.

- An explanation of how a company’s sustainability targets and KPIs are integrated in the performance incentives of the management of the company.

- An evaluation of the expertise available to the board to monitor the implementation and review the content of the company’s sustainability strategy. Such expertise should be proportionate to the complexity of the challenges facing the company, and can be ensured by board members with relevant subject matter expertise or through an advisory committee composed of independent experts and managers.

• Previous article on the reforms in corporate disclosure in 2021 including 10 key changes expected in the EU Non-Financial Reporting Directive is available here.

Filip Gregor is head of responsible companies at law firm Frank Bold. This is the second article in a series of monthly briefings on sustainability reporting in 2021. Frank Bold initiated and now coordinates the Alliance for Corporate Transparency.

Related Posts

-

February 14, 2024

Leading the sustainability transition calls for the board to go beyond compliance and ask practical questions about ESG governance.

-

July 4, 2022

‘Companies that believe their own greenwash are embedding liability and storing up risk’, warns chair of UK Environment Agency.

-

February 10, 2023

As the new rules wend their way through the EU drafting process, interested parties from all sides clamour to be heard.

-

January 13, 2022

Report suggests crisis "fatigue" is eating away at gains made during 2020, with employee issues and ESG highlighted as concerns.