On 24 May 2018, the European Commission unveiled a legislative package focused on alleviating administrative burdens on SMEs, enabling easier access to public markets for shares and bonds and increasing the liquidity of shares issued by SME growth market issuers.

According to the Commission, such transactions are expected to bring economic leverage, stronger trading in SME shares, an increase in the number of buyers and sellers and ultimately contribute to the creation of jobs and long-term GDP growth in the EU. The proposal introduces a set of targeted amendments, aimed at a more proportionate regulatory approach to support the public listing of smaller companies by amending the Regulation (EU) 2017/1129 on Prospectus; Regulation (EU) No 596/2014 on Market Abuse; and Directive 2014/65/EU on Markets in Financial Instruments (MiFID II level II measures).

As negotiations move forward in the European Parliament and Council, and decision-making reached its crucial stage, more ambition is needed in terms of recognising the diverse nature of companies in thriving EU public capital markets, and ensuring that the rules applying to smaller companies are appropriate for their size.

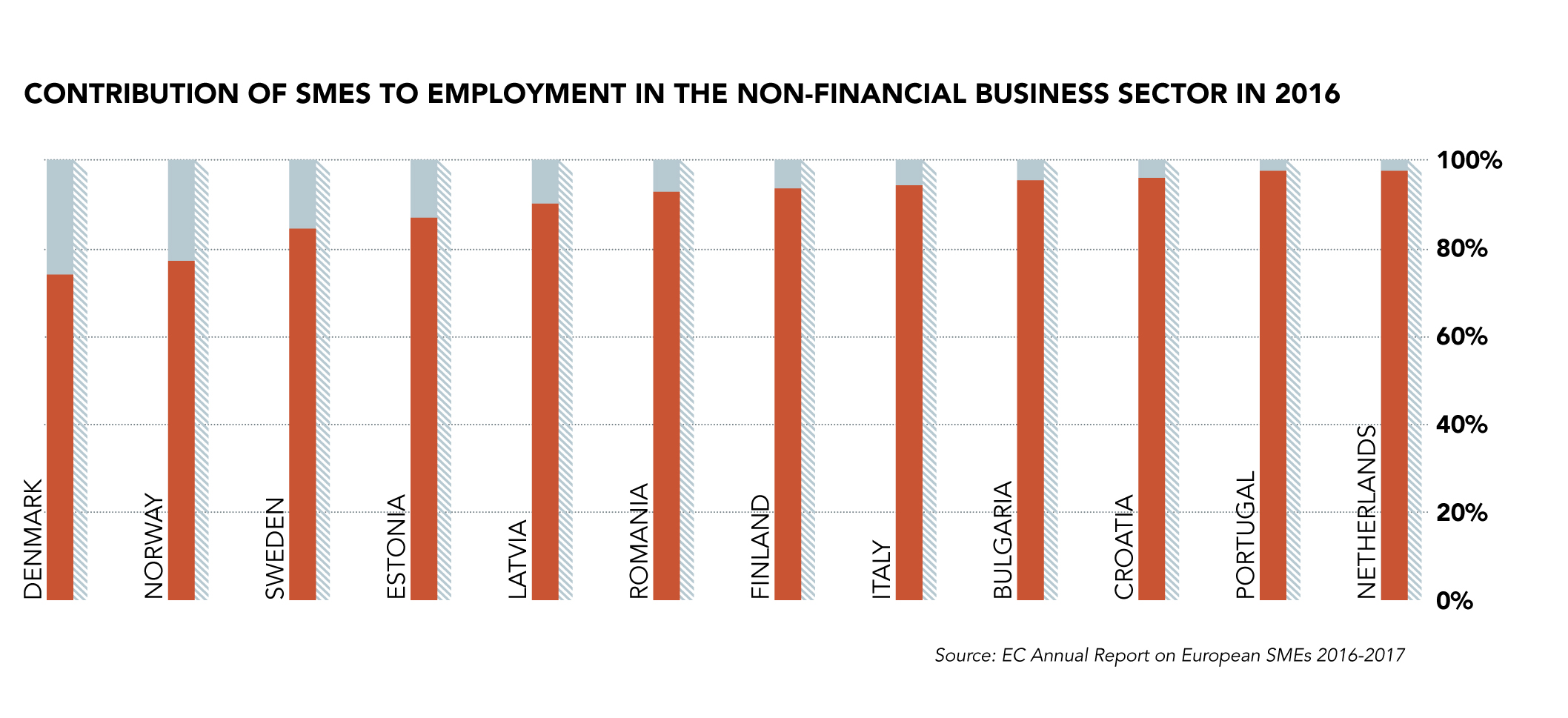

Smaller companies are the foundation of the European economy today and in the future. More than 98% of EU firms are considered to be SMEs, and they account for two-thirds of all employment (see chart) as well as nearly 60% of gross value added to the EU economy. As the basis for entrepreneurship, jobs and growth, smaller companies require a favourable environment, which meets their financing needs when accessing markets.

Small enterprises are also at the forefront of creative development. Many of these are hubs of groundbreaking innovation for products and services, especially start-up companies, often with promising high growth rates and capital returns.

However, small and mid-cap companies are fundamentally different from large blue-chip companies, as well as from SMEs (in terms of their growth potential, size, turnover, job creation, percentage shareholding of investors, and types of investors, among other things). As such, they require a different regulatory and market ecosystem, along with appropriate, tailored rules.

Clear definition

EuropeanIssuers believes that in order to recognise the diverse nature of such companies, and to help develop capital markets, a definition of a small and mid-cap company should be enshrined in EU law.

The regulatory framework could propose an upper market capitalisation threshold for small and mid-cap companies of €1bn in line with the US JOBS (Jumpstart Our Business Startups) Act as well as following the example of the French VAMPs status of listed companies with a market cap also of less than €1bn. To reflect the diversity of EU markets, member states could be permitted to adjust this threshold. European small and mid-cap companies below this threshold should be exempted from certain EU disclosure requirements and allowed to access SME growth markets.

Enhancing capital markets will improve the allocation of capital in specific market segments, facilitating entrepreneurial behaviour and investment activities. Moreover, the proposals could be a missed opportunity if the Commission does not review the criteria used to define SME growth markets for equity under MiFID II. The current threshold of €2m is extremely modest compared with the size of smaller listed companies in many member states, and should therefore be raised.

Furthermore, and even though the Commission’s intention of making corporate bond markets is worthy of praise, it is difficult to understand why some of the regulatory alleviations contained in the Commission’s proposals are restricted to bond issuance or issuers only. This is contrary to the Capital Markets Union principles of attempting to remove the bias against equity finance and extending the effectiveness of capital markets to all market players.

Tracking success is crucial for sound public markets. In September 2018, the European Parliament’s rapporteur tabled an amendment calling for the Commission and ESMA, the European Securities and Market Authority, to conduct a report focused on measuring the success of SME growth markets by the end of 2020. The report’s scope should be expanded to include data on IPOs and delistings as well as transfers of companies between trading venues. Setting up a dedicated stakeholder group with technical expertise devoted to monitoring the development and measuring success of the SME growth markets is another useful idea that is garnering the support of key Members of the European Parliament.

Flexible and transparent

Guaranteeing a flexible set of rules for transitional arrangements for small and mid-cap companies is essential. The Commission’s proposal envisages the use of a secondary offer prospectus, or “transfer prospectus” for SME growth market issuers listed for at least three years when seeking a transfer to regulated markets. Cutting this period to 18 months would allow companies to streamline their access to sources of funding and investment, turning it into a simplified “transfer document”.

This more transparent document could include useful information, such as the securities to be admitted and the rights attached, the risk factors, activities and organisation, governance and the company’s last financial report. Naturally, the National Competent Authority would have to approve the document, so that investors are protected and the standard of disclosure on regulated markets are met.

There is also a need to address the disproportionate regulatory regime and high compliance costs as major deterrents to

listing. The Commission proposals brought some alleviations for SME growth market issuers regarding market abuse rules. On the other hand, the European Parliament’s draft report proposes credible business-friendly amendments, such as the exemption of any private placement of bonds from the market sounding requirement.

Other further alleviations EuropeanIssuers proposes are:

- Adjust the deadline to publicly disclose managers’ transactions of companies on SME growth markets from three to two days, as well as extending such provision to companies listed on other MTFs (multilateral trading facilities) and regulated markets

- Exemption of smaller listed companies, or at least those on SME growth markets, from the obligation to draw up and keep lists of persons closely associated with a director or a senior manager

- Sanctions should be effective and dissuasive but also proportionately fair, as current thresholds are disproportionally higher when compared with the market capitalisation of many smaller listed companies.

Fines concerning the failure to settle trades on time from securities of all companies on SME growth markets and small and mid-cap companies irrespective of trading venue should also be removed.

Next steps

What are the next steps? The European Council’s working party on financial services is still discussing the proposal. The European Parliament’s course of action is in a slightly more advanced stage. Its draft report is expected to be voted on during the ECON (Economic & Monetary Affairs) committee in December 2018, and adopted in plenary by the first quarter of 2019.

Also in December, EuropeanIssuers co-organised the EU Small and Mid-Cap Awards Gala dinner, the annual ceremony which celebrates small and mid-cap companies in Europe. The event highlights the diversity of European markets, promotes best practices and showcases the most successful IPOs of EU companies according to their results in terms of international sales, profit, market share growth and innovation.

Florence Bindelle is secretary general and Frederico de Santos Martins is policy adviser at EuropeanIssuers.

Related Posts

-

March 4, 2022

Difficulty of due diligence on sanctions intensifies, as a host of companies around the world withdraw from Russian investments.

-

August 6, 2021

As UK government proposals increase responsibilities for directors, our latest podcast discusses the impact on internal controls and dividends.

-

October 5, 2021

Transparency groups including Greenpeace UK say failing to disclose the audits involved "risks creating a general lack of confidence in all audit opinions".

-

August 23, 2021

All-Party Parliamentary Group argues for greater transparency around tax deals struck by HM Revenue & Customs (HMRC) and big corporates.