The statistics make it plain. Activist investors are having an impact on boardroom decision-making, with increasing regularity.

And none more so than in the UK, where the “threat” of activism has increased in the past year. Activist action is 46% more likely to affect a UK-listed company than its peers in Europe, according to Alvarez & Marsal’s Activist Alert research.

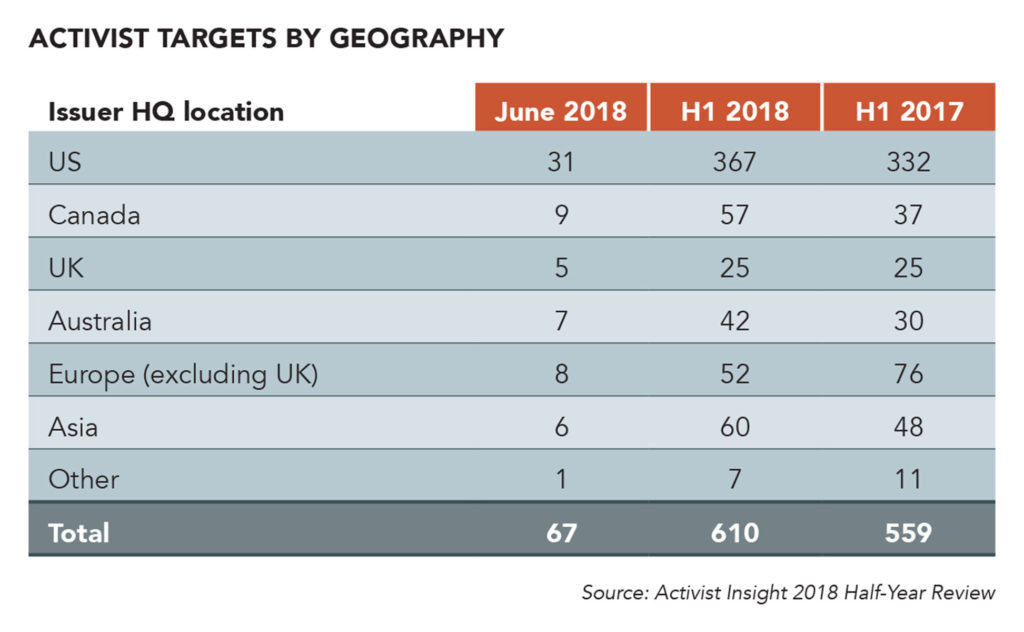

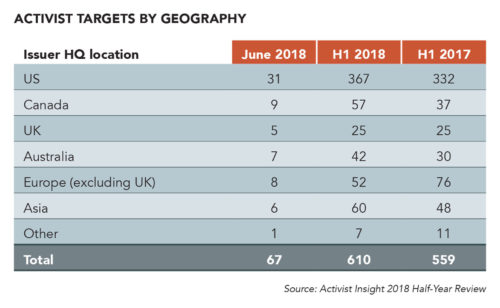

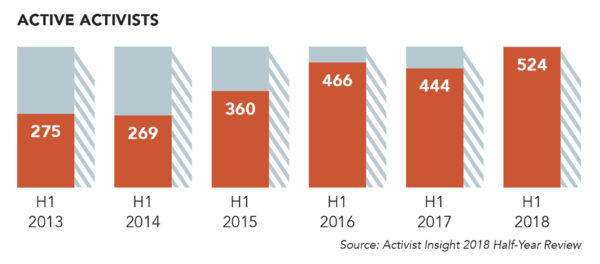

But it’s not solely a UK phenomenon. A global study by Activist Insight found 524 investors making public demands of companies in H1 2018, compared with 444 a year earlier.

Reasons

Reasons

For Malcolm McKenzie, Alvarez & Marsal report co-author and head of its European corporate transformation services practice, the reasons why the UK tops the activism chart is threefold.

Firstly, it’s the largest listed market in Europe, with the most liquid stocks. Secondly, board governance rules are “shareholder-friendly”, more easily enabling the requisition of an EGM or proposal of a resolution. Thirdly, a lot of activism derives from US-based investors, and alignment of language and legal structures between the two jurisdictions pushes the door wide open.

While activism is still growing, it’s “no longer immature”, says McKenzie. “We might have said that three years ago that people were still finding their way. Now, it’s pretty mainstream. In the UK it’s an accepted part of the market environment.”

Second generation

And this maturity is bringing about a range of behaviours. Josh Black, editor-in-chief at Activist Insight, sees what he calls the “second generation” of activists, with the old guard becoming bigger and broader. “Take Elliott for example, they now have 15 situations across three continents. These organisations are becoming an attractive place for management consultants and investment bankers to go and work.”

Another term that is on the rise in activist parlance is that of “wolf packs”. For Alvarez and Marsal managing director Paul Kinrade, the next level of maturity in activism has seen investors building a consensus of opinion before approaching a board, “not just banging on the door”.

Another term that is on the rise in activist parlance is that of “wolf packs”. For Alvarez and Marsal managing director Paul Kinrade, the next level of maturity in activism has seen investors building a consensus of opinion before approaching a board, “not just banging on the door”.

“In the early days of activism in the UK, activists came with an approach that was clearly short-term focused, and their [ideas] thrown out by existing shareholders. The idea is to become a wolf pack of like-minded investors.”

Ultimately, activism needs to be judged by its impact. Has it “improved” companies?

McKenzie is clear that activism has driven value. He cites the Alliance Trust battle between the company’s board and activist shareholder Elliott. Alliance’s board once claimed that Elliott “threatens the very existence of the company” before buying out its shareholding; for McKenzie it is clear that activism “changed the model and management approach, driving value”.

Leverage

Much investor ire has focused on executive remuneration and its alignment—or lack of it—with the creation of long-term value. Activism hasn’t in itself driven better governance, McKenzie believes, but governance and codes can be used as leverage to mount an attack.

“Don’t kid yourself, the [activists’] game isn’t driving better governance, it’s about driving value, and the code is a lever,” states McKenzie.

For Black, activism can help businesses in the long term by “removing complacency and forcing a company to address its business model”.

McKenzie adds: “Activists can challenge the board by saying ‘you’re not going fast enough or slow enough’. They’re a helpful part of that environment.”

The challenge for boards is gaining a “robust understanding” of their market and setting a coherent strategy, “taking on board all the potential challenges to drive that value”, says Kinrade.

“If you’re in the position to understand how you drive performance against peers—it will ‘tick the box’ for long-term activists,” Kinrade concludes.

Kevin Reed is news editor at Board Agenda.

Related Posts

-

October 14, 2022

Decarbonising 'brown' industries; funds pulled from BlackRock; the legitimacy of dual class shares; investors slow to address sustainability.

-

June 17, 2022

Researchers say firms may exaggerate their ESG performance over fears that investors will divest from their stock.

-

November 2, 2021

Research suggests a decrease in quarterly reporting is linked to decreased company value—and impacts smaller firms more than larger firms.

-

February 25, 2022

Investors will be "assertive" in 2022; Carl Icahn fights for animal rights at McDonald's; and childhoods spent in nature make greener CEOs.