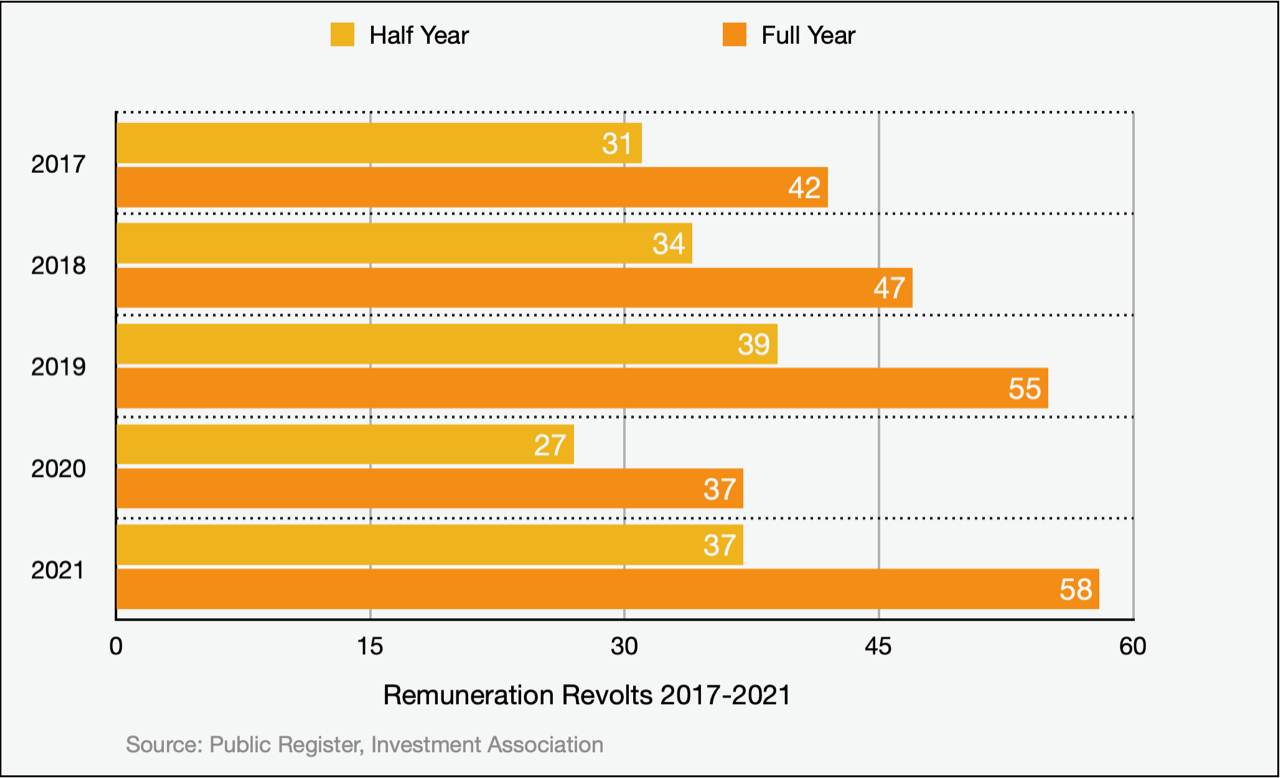

Shareholder revolts against UK remuneration reports increased significantly last year, up 56% on 2020. The rise represents the highest number of notifiable shareholder revolts on pay for five years.

The figures suggest that investors are willing to maintain the pressure on companies over pay levels despite concerns some shareholders may be losing interest in excessive executive pay.

Board Agenda analysis shows there were 58 shareholder revolts against the remuneration reports of listed companies in 2021, based on a 20% threshold for registration of an opposition vote on the Public Register maintained by the Investment Association.

Pay revolt numbers in 2020 dipped to 37 as shareholders eased the pressure on boards during the first year of the pandemic, though many warned chief executives that they should share the pain experienced by workers who either saw themselves out of work on furlough or with reduced pay.

That said, 2019 saw pay revolts rise 17% to 55, a year in which shareholder worries about executive pay appeared to reach a peak. However, the number of pay revolts has been rising each year since 2017, a clear indication that executive pay remains high on the agenda of investors. At the half way point, 2021 already had as many pay revolts as the whole of 2020.

That is likely part of wider concern with ESG (environmental, social and governance) topics. High pay levels are often viewed as an indicator that attention to ESG subjects at a company may be an issue.

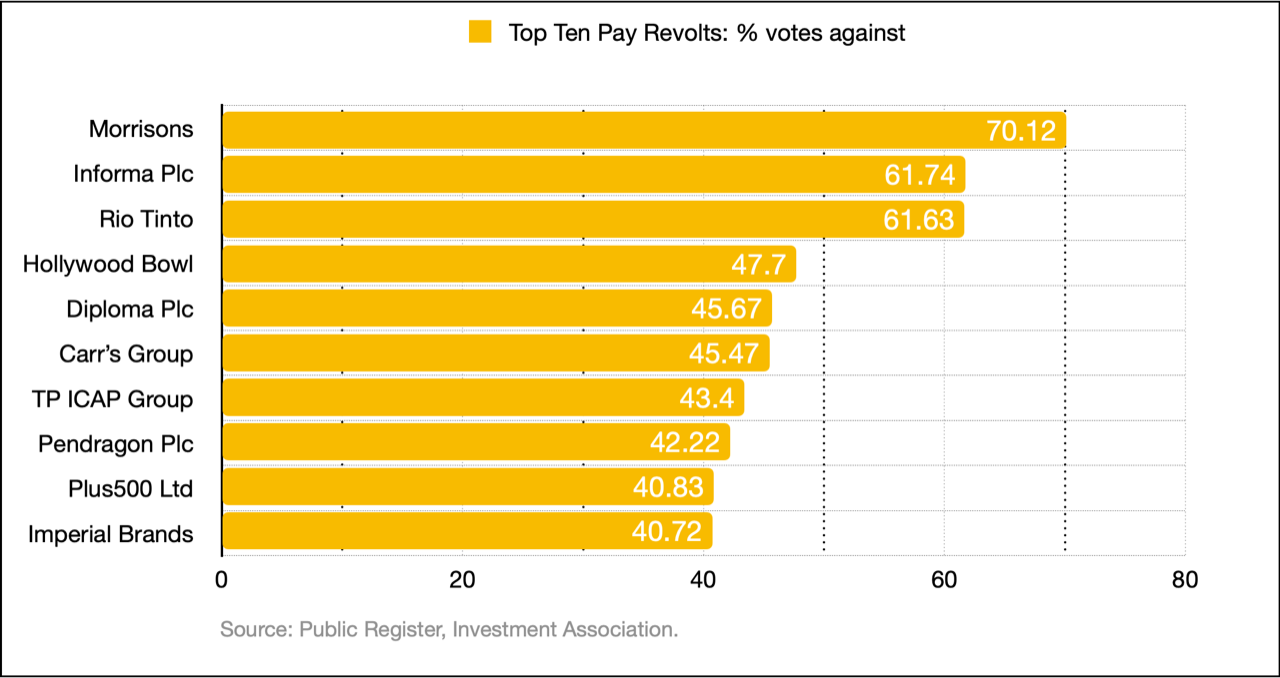

Big names face pay revolts

Last year the biggest pay revolt was against the remuneration report of supermarket group WM Morrison, which saw 70.12% opposition to its executive pay deals.

The day after the vote Morrison said it had attempted to explain the pay deal maths to shareholders, and its performance during the pandemic, ahead of its AGM in June.

“In the [remuneration] committee’s view,” a company statement said, “Morrison performed exceptionally well for the nation during the first year of Covid with the executives widely recognised for their leadership, clarity, decisiveness, compassion and speed of both decision-making and execution. Almost overnight, the entire business effectively re-positioned to feed the nation and to make sure no-one was left behind.”

Another company on the sharp end of a shareholder protest was media outfit Informa Plc, with a 61% vote against its remuneration report. In a statement after the AGM the company said it would “initiate a new consultation with shareholders on its next approach to remuneration”. That consultation was expected to happen ahead of this year’s AGM.

A third organisation to fall foul of remuneration rumblings was mining giant Rio Tinto, which also saw 61% of shareholders turn on its pay arrangements.

Elsewhere, Hollywood Bowl, a chain of bowling alleys, acknowledged investors’ 47.7% vote against the board’s remuneration report. The company said the point of concern was the use of a Long Term Incentive Plan (LTIP). The company said it would continue to engage with investors and “respects the views expressed by shareholders regarding this resolution”.

This year has already seen a crop of major shareholder revolts, including at publishing house Future plc, where more than half of shareholders votes (55.44%) objected to the remuneration report. The company said it would embark on a “new consultation process with shareholders” after noting concerns including those with the departure deal for former finance chief Rachel Addison.

WH Smith, the High Street news agent, suffered a big revolt in January, with a 45.60% vote against its pay report.

LGIM and executive pay

Despite some fund managers insisting that excessive pay remains an issue, news reports in November suggested one fund manager, Legal & General Investment Management (LGIM), was giving up on pay engagement because its views were being ignored.

Angeli Benham, senior global ESG manager at LGIM, says engagement on pay has continued with boards and the 2021 spike in pay revolts was likely caused by fund managers applying their own policy, or that of the Investment Association, that companies that had taken pandemic loands from government or had to resort to “emergency capital” from shareholders, should not pay bonuses.

She adds that after two years of “no bonus”, or LTIPs failing to vest, there has been a rise in the number of boards seeking to “apply discretion” on payouts. This may, in turn, cause an uptick in the number of votes against remuneration reports in 2022.

“Executives should be paid for being good stewards of their company, for ensuring that when they operate, they do not negatively impact the environment or other stakeholders and for delivering long term growth and value for its shareholders,” says Beham. “It has been a difficult task over the past two years for many executives to navigate unchartered waters caused by the pandemic and difficult decisions were taken to ensure their business remains a going concern.

Sandy Pepper, a professor and expert on executive pay at the London School of Economics, says investors face “a collective action problem”, as differences in policy emerge. Norges Bank, for example, the Norwegian sovereign wealth fund, has said it wants LTIPs done away with entirely.

“Nevertheless,” Pepper says, “there have been signs in recent years that institutional investors are increasingly taking their oversight of executive pay more seriously.”

Investors paid attention to executive remuneration last year, delivering a record number of pay revolts. They’ve already begun this year and are likely to continue.

Related Posts

-

July 2, 2021

Analysis by Board Agenda reveals that pay revolts in the first half of 2021 are up on the same period last year by 51%.

-

September 7, 2021

Spain saw the greatest opposition to remuneration-related resolutions, with 60.6% contested—an increase of 33.2% year on year.

-

September 21, 2023

Very few investors use their AGM votes on executive pay as a spur to improve the company’s ESG performance, research shows.

-

March 28, 2022

A report from EQ forecasts the big topics in this season's AGMs, and underlines the need to get out of reaction mode.