Why, indeed, are executives paid so much? You must have asked yourself that question.

If you are a member of a Remuneration Committee, you have probably been paid to ask that question.

By their own admission, firms like WPP in the media industry and the Berkeley Group in property pay very large sums. According to its 2014 annual report, the CEO of WPP was paid the sum of £42,978,000 for one year’s effort on behalf of his shareholders. The executive chair of the Berkeley Group, according to its 2015 annual report, received the sum of £23,296,000. These are not complete outliers—there are many similar examples.

But the answer to “how much is too much?” is not so easy to give. Not least because the companies and the shareholders from the firms mentioned above and elsewhere would themselves argue that incentive pay works and the pay was “worth it”. While executives and their pay is an age-old debate that sells papers and enables politicians of every hue to take a stand, the only thing those parties agree about is that “something needs to be done”.

We believe that is largely because people have focused on the cost of executives not their value.

Based on several years’ worth of research, we can inject some fresh thinking on the debate.

- We can tell you whether an executive is worth it.

- We can tell you what they will have to do to justify their package.

- We can tell you what you must do, and what you should avoid doing, as a remuneration committee member.

Is an executive worth it?

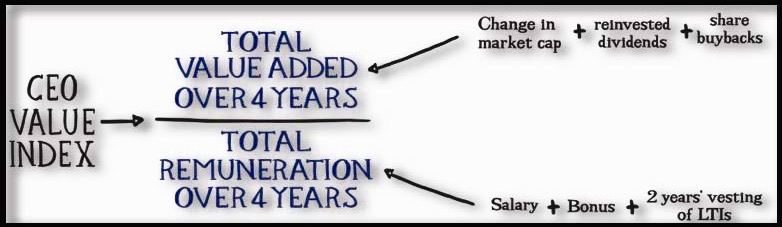

We developed a simple index which looks at how much value is added to the company per £1 of compensation paid to the CEO over a four-year period. This is the “UK CEO Value Index” (below).

Conducting our research over a longer time frame helps to recognise long-term value creation for shareholders, and captures any pay deferred through longer vesting periods.

The Index gives a simple rule-of-thumb guide to pay and performance, as well as a guide to the future value CEOs must deliver if they are to justify their pay packages.

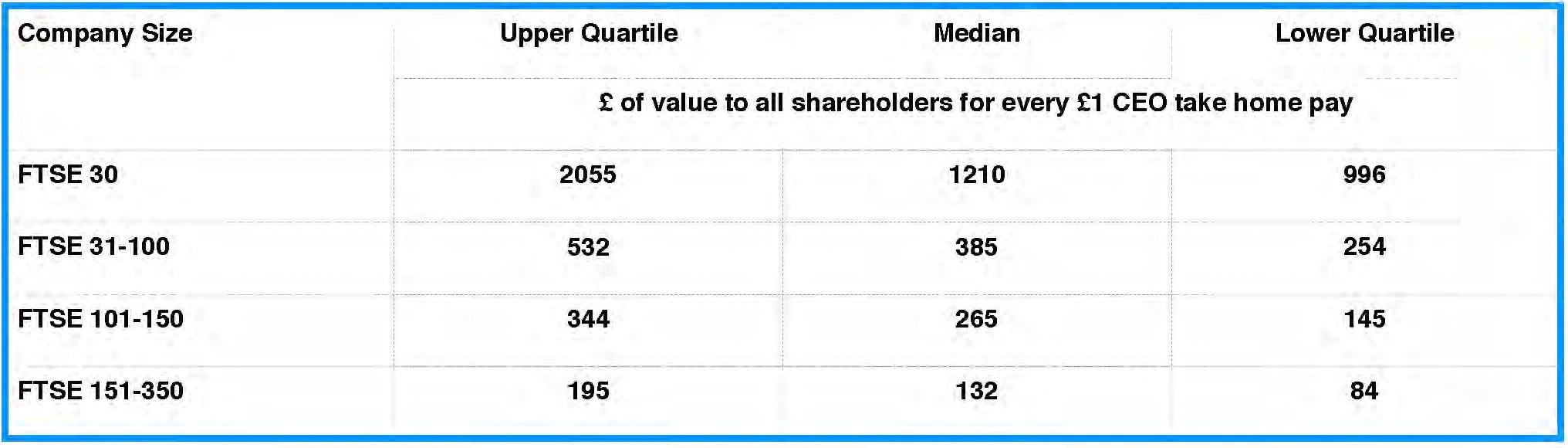

We’ve found that 90% of the companies surveyed on the FTSE 300 deliver less than £1,000 for every £1 paid to the CEO.

Given that we are looking at over 27,000 pieces of pay and performance data over four years, the outcome is a surprisingly narrow field. More than half (52%) of all FTSE 100 companies studied deliver between £240 and £740 to all of their shareholders for every £1 paid to the CEO—a range of just £500. Seventy-one percent deliver within a £1,000 range of £210 to £1,210. With regards to the FTSE 250 alone, nearly half (47%) of these companies are within an even narrower range of Index outcomes, between £58 and £158.

2015 CEO Value Index Scores

If we return to our original list, how did they do on the 2015 CEO Value Index?

WPP: Index of £201

Berkeley Group: Index of £142

We also have an example of the range of Index scores among similarly paid CEOs. In this case, all three earned between £11m and £12m in 2014–2015.

Reckitt Benckiser: Index of £574

Prudential: Index of £875

Betfair: Index of £268

There we have the answer to the question: are they worth it? This is a powerful tool that remuneration committee members can use when making remuneration decisions.

What does a CEO have to do to justify their pay?

Are investors happy that the majority of pay programmes deliver less than £1,000 for every £1 paid to the CEO?

The upper quartile index figure for the FTSE 100 is just over £1,000.

If you are a member of a FTSE 100 remuneration committee, here are some interesting facts:

- The FTSE 100 company which actually sits at the upper quartile of the index has a four-year total value added of £7.8bn and total remuneration of £7.8m.

- Upper quartile pay for a FTSE 100 CEO (“the market”) over four years is £16.1m.

- A company paying at the upper quartile total remuneration level of £16.1m, and aspiring to deliver an index score of over £1,000, will need to add £16bn in shareholder value over a four-year period.

This means, as a remuneration committee member, you can spend less time on “market” pay figures—take those as a given—and more time on what must be delivered, and how, to justify “market” pay.

What can you do, as a member of a remuneration committee?

How are we to respond to this challenge?

- Don’t throw out long-term incentives. Our research shows that the element of pay that most clearly aligns the investor’s experience with that of management is in the area of long-term pay. While share price may be a “vote” in the short term, it is reflective of the underlying success of the company in the long term. It is true that long-term incentives are unpopular amongst executives, but that is because too little long-term pay is tied to the operational performance that management is actually responsible for.

- Annual bonus should form a lower proportion of overall pay. Our research shows that in the past ten years bonus opportunity for the same performance has risen markedly. This cannot be right, but it is—sadly—the unintended consequence of investor and government initiatives to place Total Shareholder Returns (TSR) at the centre of incentive programmes in the UK. Measuring TSR relative to others, or even on its own, is a fickle guide to management’s success. Quite simply, it is almost impossible for the best-run company to out-perform median TSR more than six times out of ten. So, for those four years the best managers in the best-run companies scratch their heads and say to themselves that it is only annual bonus that really matters to them.

- Investors must tolerate more not less discretion in pay programmes. It is clear from our research that the increasing complexity of performance conditions has a downside. Both investors and participants are confused as to how performance translates into pay in the future, because we do not know the future. It cannot be in the interests of shareholders to focus on a particular performance requirement when, as we have shown, it is that £16bn of incremental value for all shareholders—however it is delivered—that really matters.

- Companies should aspire to deliver more than £1,000 per £1 of CEO compensation. With that simple rule in mind, everyone could spend less time commenting on executive pay and more time on the strategy needed to deliver improved value for shareholders.

What else you should know?

- We found that salary still plays a very large part in CEO pay packages.

- Among the FTSE 350 overall, over four years, median salary amounts to more than both median cash bonuses and vesting LTIs.

- Size does drive pay. The FTSE 30 has consistently higher remuneration than the FTSE 31–100 over the four-year period.

- There are a significant number of outliers and a considerable cluster of companies that appear to be delivering the same value but awarding very different remuneration. Interestingly, companies that have lost value are not awarding the least pay, nor are those delivering the most value awarding the most pay.

- While a CEO’s salary is not strongly linked to the value added, FTSE 30 companies consistently deliver the most value to shareholders and pay higher salaries.

- There is a large group of companies delivering similar total value added, but awarding vastly different cash bonuses ranging from £0 to £11m over the four-year period. Those companies that lose value are often awarding cash bonuses that exceed those received by CEOs delivering positive value to shareholders.

- Where there is a clear link between incentive compensation and performance, it is the link between long-term incentives and the value added to the company.

What to do next?

As a remuneration committee member, give serious consideration to the use of a decision tool like the UK CEO Value Index. Exploring where your company might rank in the distribution and understanding your peers’ positions can help provide a more rational guide for decision-making—one that will better align the performance of an executive to the long-term interests of shareholders.

Simon Patterson is managing director of Pearl Meyer.

Related Posts

-

July 1, 2021

Researchers have interviewed non-executive directors and investors to highlight the hidden factors involved in CEO pay decisions.

-

November 16, 2021

Incentive plans, share awards and bonus payments have become almost a guaranteed part of a chief executive’s pay package.

-

April 11, 2023

Investors are likely to focus on top pay in this year’s AGM season, as research reveals that executive pay has bounced back.

-

October 8, 2021

South Africa has the highest wage inequality in the world, and there is growing interest in remuneration governance and director pay.